Input Cost Shocks

16 March 2026

The conflict in the Middle East through the first weeks of March has reintroduced a high degree of volatility across global energy and fertiliser markets, reminding agricultural supply chains how quickly geopolitical events can influence the cost of key farm inputs. Australia’s heavy reliance on imported energy will be a hotbed discussion topic for the future, however for the here and now we will examine the potential real impacts on Australian farming businesses in the near term.

In particular, diesel and nitrogen fertiliser have both experienced sharp price increases as production and logistics constraints in key exporting nations is translated into Australian pricing. As a pool manager at Advantage Grain, it is imperative to be fully aware of all costs associated with each trade. Whether it be BHC costs, logistics costs or financing costs. However, cost of production and sensitivity to input changes is something that is sometimes overlooked by grain buyers (growers are more than aware). The below report focuses on a sensitivity model to show the impacts outsized price swings have on a per tonne basis for the average Australian grower.

Diesel: The unavoidable operating cost

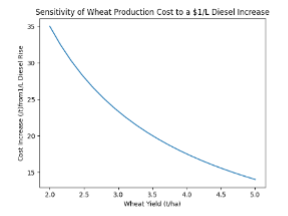

Diesel sits at the centre of almost every farming operation. From seeding and spraying through to harvest and grain carting, it is one of the few inputs that cannot easily be substituted or deferred when conditions demand action. Storage and longer-term supply agreements are becoming more common to give growers limited price risk management, however for the most part growers are exposed to market fluctuations.

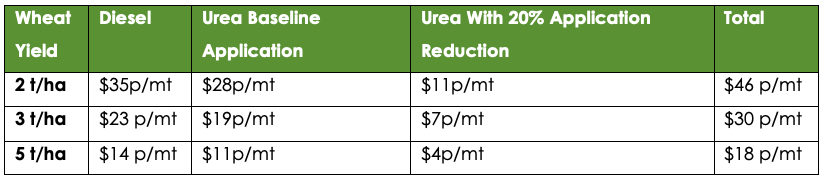

Across a typical Australian wheat program, diesel consumption generally falls in the range of 55–80 litres per hectare[1] (L/ha) once seeding, spraying, fertiliser spreading, harvesting and in-field logistics are included. Using a midpoint of roughly 70 L/ha, a $1/L increase in diesel equates to an additional $70/ha in operating costs.

Converted to a production cost per tonne, the impact varies significantly depending on yield:

- Low rainfall zones (≈2 t/ha): ~$35/MT

- Average production regions (≈3 t/ha): ~$23/MT

- High yielding regions (≈5 t/ha): ~$14/MT

Nitrogen: balancing cost and yield

Nitrogen fertiliser is typically the largest single input in wheat production. For this analysis, consider a representative program of 140 kg/ha urea applied for nitrogen.

Using a baseline price $800/MT for urea, this program equates to roughly $187/ha.

If urea rises to $1,200/MT, fertiliser costs increase to approximately $243/ha — an uplift of around $56/ha.

Expressed per tonne:

- 2 t/ha: +$28/MT

- 3 t/ha: +$19/MT

- 5 t/ha: +$11/MT

These lofty prices will of course lead to demand destruction and growers seeking alternative sources of nitrogen. Assuming a 20% reduction in urea application lowers costs to roughly $209/ha, narrowing the net increase to around $22/ha.

Beyond the Farm Gate

Further down the supply chain the costs are lesser but still meaningful, rail transport typically consumes around 0.7 litres of diesel per tonne of grain on an average sized train doing a 300km journey, meaning a $1/L move in diesel prices lifts rail freight by roughly $0.70/MT.

Road freight is more sensitive with much more drastic consequences, averaging around 3.5–4.0 L/t. Under the same diesel scenario, this would lift road freight costs by approximately $3–4/MT.

The overall impacts of these ballooning freight costs will be felt in the market at all levels; the road freight dropping a load to the local silo or feedlot, or the panamax taking 60,000MT of Australia’s finest to one of our global customers.

Implications for the Global Grower

As it stands, this input shock is both meaningful and when combined, these inputs could lift wheat production costs by A$18–46/MT across many Australian regions, particularly in lower rainfall areas at a time when growers are already operating very close to or below cost of production. These cost pressures are not unique to Australia, with global growers facing the same pressures.

The other side of this equation is grain pricing. When fertiliser and fuel costs rise sharply, the marginal hectare in many producing regions can quickly become uneconomic. In these situations growers will reduce planted area, switch into lower input crops, or simply avoid pushing production on less productive ground. While these decisions occur farm by farm, the cumulative effect across major exporting regions can lead to a meaningful contraction in global acreage and production. Even modest reductions in planted area can tighten the global balance sheet, and then it is the job of the market to ration stocks, push prices higher and incentivise production.

Australian growers are among the most capable and resilient in global ag. Input price volatility is never welcome, but it is also not new. The industry has navigated far more challenging cycles before; droughts, floods, fires, pandemics and global financial shocks to name a few. We hope the conflict in the Middle East can come to a swift end so growers can focus on the more important things (planting crops and Sydney Swans winning a flag). Good luck to all over the next weeks with your inputs and fingers crossed for some more rain.

[1] Diesel burn rate estimates are based on studies published by Grains Research & Development Corporation (GRDC), NSW Department of Primary Industries, Agriculture Victoria, Department of Primary Industries and Regional Development.

Share This Article

Other articles you may like